Groupthink Sets in at Powell’s Federal Reserve

Dissents dwindle along with viewpoint diversity

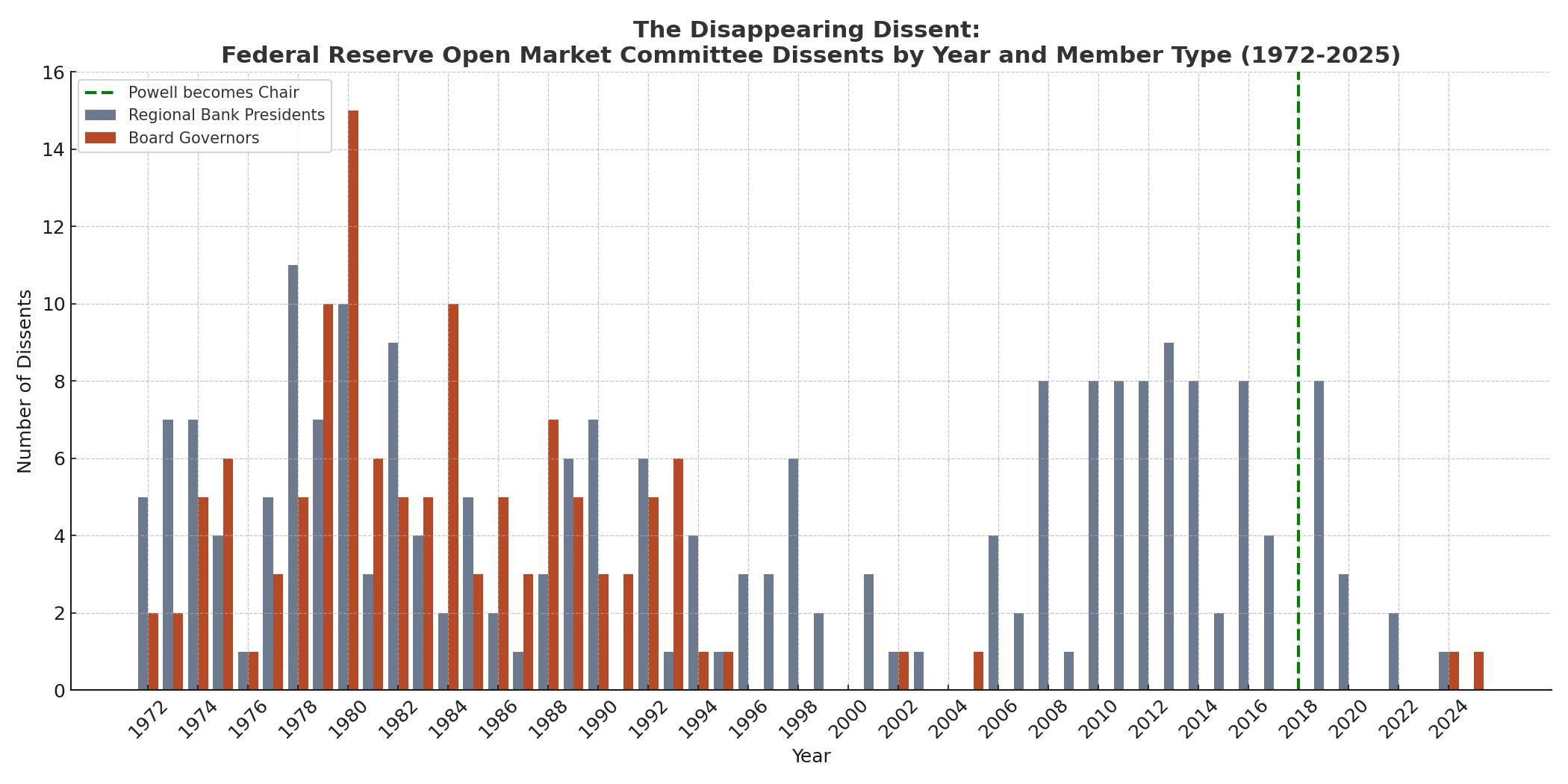

The Federal Reserve Bank of St. Louis maintains a blog post from 2014 headlined “A History of FOMC Dissents.” The charts only run through 2013. Since then, the history has been largely unwritten, a testament not only to increasing unanimity on the Fed Open Market Committee, but to a loss of the intellectual energy and viewpoint diversity that used to be a feature of the Federal Reserve structure, and especially its regional banks. It’s not just about the missing dissent votes: it’s about the absence of ideas.

I’ve brought the chart up to date here as a graphic illustration of how ideological conformity set in at the Federal Reserve during Chairman Jerome Powell’s leadership, a period that also included one of the biggest monetary policy errors in the past half-century—a slow and late reaction to Bidenflation that kept the federal funds rate at zero all the way into March 2022 when Consumer Price Index Inflation was at 8.5 percent.

Some voices around the Fed are beginning to push back against Powell’s iron grip.

A July 2023 paper by Gauti Eggertsson of Brown University and Don Kohn of the Hutchins Center at Brookings noted, “the years 2021 and early 2022 were extraordinarily difficult times for policymaking in which the path forward to accomplish the Federal Reserve’s dual mandate was not clear and subject to different judgments. Yet no FOMC voters dissented between September 2020 and June 2022, raising questions about whether Committee discussions and decisions were being sufficiently challenged by diverse viewpoints….The FOMC has had a very consensus-driven decision process. The Committee should ask itself whether different aspects of its decisions and decisionmaking are allowing sufficient scope for effective challenges to the majority view.” Kohn is a former vice chairman of the Fed Board of Governors.

A February 2024 podcast featuring the former president of the Richmond Fed, Jeffrey Lacker, included Lacker talking about how Fed governance has changed. “A lot of us back then were relatively outspoken, were willing to speak in public and describe alternative perspectives on the current policy outlook, describe different points of view about where policy should go,” he said. Then the Fed Board of Governors started taking a stronger role in hand-selecting the regional bank presidents. Said Lacker, “The Board will steer them away from certain candidates…does that, in some way, filter out people that just have diverging views, legitimate alternative perspectives on the way policy is conducted? I suspect it has.”

Said Lacker, “I suspect that that’s led to the selection of people that, on the whole, have a stronger alignment with the Board of Governors’ views. And, in addition, less of a propensity to express dissenting views, at least outside the committee. That's my conjecture about the governance process, that it's shifted, and we can talk about why. But that's something, I think, that's happened over the last decade and a half.”

When I wrote about the Lacker podcast recently (“For Fed Chairman Powell, a Paradox,” April 8, 2025), I got a note from a reader, Noam Neusner, who said in part, “I am sympathetic to your point about the control now wielded over the regional Fed banks. When I covered the Fed for Bloomberg in the 90s and 00s, the Dallas Fed was always known as a center for free market thinking, in contrast to ALL the other regional banks – their bank president gave speeches that were outstanding examples of Hayekian thinking. Some of the other regional bank presidents were, however, quite iconoclastic, or at least independent-minded. Hoenig in Kansas City. Poole (a former Brown professor) in St. Louis. If the regional banks are becoming less distinctive, reflecting the regional concerns of their districts, that’s a real loss for policymaking. Even the Boston Fed stood out for its distinctive thinking. I remember a conference at Bard… that focused on Hyman Minsky (whose thinking and ideas deserve attention at this very moment!), and it was attended by several Fed Bank officials and presidents. The rotating members of the FOMC who are regional bank presidents always represented the most common source of dispute within the Greenspan Fed. As a reporter, you could glean quite a bit from following regional bank presidents, their speeches, and even the research published by their journals. If the FOMC has squelched this relatively rich diversity of intellectual and policymaking curiosity, it’s a great shame.”

The value of the regional Fed banks has been well documented in academic literature. A 2019 National Bureau of Economics working paper by Michael Bordo of Rutgers and Edward S. Prescott of the Federal Reserve Bank of Cleveland argues that “the Federal Reserve’s decentralized structure was favorable to the processing and generation of ideas, that the Reserve Banks were an important entry point for new ideas into the Federal Reserve System, and that these ideas ultimately contributed to Federal Reserve policy making.” As they put it, “A central bank that is structured so that it can learn new ideas will be better able to solve problems as they arise and will be more effective.”

Early on in Fed history, the regional banks even attempted their own, independent, monetary policies. As Bordo and Prescott recount, in 1927 Benjamin Strong, who headed the New York Fed, went so far as to meet on Long Island with the central bankers of England, France, and Germany, and agreed “that the New York Fed would lower its discount rate to help the Bank of England in its struggle to stay on the gold standard.” In 1933 the New York Fed asked for a temporary loan of gold from the Chicago Fed, which turned New York down, fueling a panic.

The St. Louis Fed, beginning in 1958 under research director Homer Jones, who had taught Milton Friedman economics at Rutgers, became a center for Friedman-style monetarism. As Bordo and Prescott put it, “the St. Louis Fed adopted Friedman’s quantity theory views and emphasized monetarist signals for evaluating policy,” not only via its president, but via a research department with “close ties to leading academic monetarists such as Karl Brunner, Milton Friedman, Alan Meltzer, and Anna Schwartz.”

The Minneapolis Fed, meanwhile, “became closely associated with and was a major contributor to the rational expectations revolution in macroeconomics that started with Robert Lucas,” as Bordo and Prescott recount. “The Minneapolis Fed’s connection to rational expectations started in 1970 when John Kareken, a professor of economics at the University of Minnesota and an adviser to the Minneapolis Fed, formed a group to build an econometric model in which to derive optimal policy rules.”

Bordo and Prescott also talk about the contributions of the Richmond Fed on transparency and the Cleveland Fed on inflation targeting. “The anti-establishment ideas of the 1970s that were tied to several of the Reserve Banks influenced policy and were successful at controlling inflation,” they write.

“We are unaware of any such entity in which public disagreement is tolerated to the extent that it is tolerated by the Federal Reserve. The short-term incentives for most agencies (as well as many other organizations) are to keep all debates internal and then present a united front to the public in order to prevent outsiders from using these divisions against the agency. We think the long-term costs of that type of behavior for a central bank are significant. It leads to filtering of information and groupthink and can make it difficult for an organization to learn,” Bordo and Prescott conclude in a caution that now seems prophetic.

A 2021 paper by Christina Parajon Skinner of Wharton and Carola Binder of the University of Texas at Austin, Laboratories of Central Banking, traces the regional Fed banks back to a congressman from Virginia, Carter Glass, who said the Federal Reserve system “is modeled upon our federal political system . . . . The regional banks are the states and the Federal Reserve Board is the Congress.”

“Each Reserve Bank, in turn, has further developed an identity around specific issue areas,” Skinner and Binder wrote. Skinner and Binder looked at all 4,871 working papers published by the twelve regional Reserve Banks from January 2006 through December 2021 and found an increasing focus on race, gender, climate, and inequality.

When thoughtful people look back at troubled eras in monetary policy, a failure to listen to different views is a recurring theme. Kohn, in an oral history for the Fed, talks of Arthur Burns, who was Fed chairman during the stagflation period of 1970 to 1978: “He didn’t tolerate diverse views and therefore didn’t hear the kinds of views and opinions that he needed to hear and the Federal Reserve needed to consider at what was a difficult time for the Federal Reserve System—at a time, in retrospect, in which we obviously could have done much better with our monetary policy.”

The interviewer asked Kohn, “Do you think the country is well served by having, say, a St. Louis Reserve Bank with a monetarist tradition and other Reserve Banks with their various traditions so that, when you get to the FOMC meetings, the Committee is getting these different Perspectives?” Kohn replied, “It’s good to have diverse perspectives on the FOMC even when I disagree with them. It’s good that these people bringing these perspectives have their own independent research functions to help them think the stuff through….the fact that the Reserve Banks form a natural avenue for diverse policy views to be heard in the Committee is a good thing.”

The personnel do exist if some regional bank wanted to elevate an unconventional president or if President Trump wanted to insert an unconventional governor. Ask John Cochrane, George Selgin, Lawrence H. White, or Jim Grant for ideas. President Trump’s Monday April 21 description of Fed Chairman Powell as “Mr. Too Late, a major loser,” is blamed for scaring the stock market yesterday, and Trump gets described as a would-be autocrat who can’t tolerate Powell’s supposed independence.

Yet the big “no dissent” stretch at the Fed ran from September 2020 to June 2022, a period that spanned two presidential administrations and included the inflation that was so politically damaging to Biden and his vice president. Fueling the Powell-Trump drama and the related stock-market gyrations is a longer-term story with longer-term implications that will outlast any single day’s market results. It’d be a fertile topic for consideration and perhaps even some adjustments by Congress. It is Congress, after all, that created the Fed with legislation. And it is Congress to which the Constitution grants the enumerated power to coin money and regulate the value thereof.