For Fed Chairman Powell, a Paradox

Best move for institutional independence may be listening to President Trump

Imagine being the chairman of the Federal Reserve, Jerome Powell. You’re trained as a lawyer, not as an academic economist like your predecessors Janet Yellen, Ben Bernanke, or Alan Greenspan. President Trump was the one who originally nominated you as chairman back in 2017, but President Biden reappointed you. Trump is not exactly your fantasy of a perfect president, or anything close. Most of the Fed staff, most of the people who live in and around Washington D.C., voted for Kamala Harris. And that carries some weight, because if there’s any word that best describes you, it’s an institutionalist—someone who cares about the Fed’s reputation and wants to defend it as an independent institution, in much the same way Chief Justice Roberts is with the Supreme Court at the other end of the Mall in Washington. This is less economics than it is political science; as James Q. Wilson observed, what motivates government executives is the desire for autonomy.

Now your prized autonomy is under attack. President Trump has been publicly pushing you for a rate cut. On April 4 Trump posted to social media, “This would be a PERFECT time for Fed Chairman Jerome Powell to cut Interest Rates. He is always ‘late,’ but he could now change his image, and quickly,” Trump said. “CUT INTEREST RATES, JEROME, AND STOP PLAYING POLITICS!” On April 7 Trump posted again: “the slow moving Fed should cut rates!”

The knee-jerk response of any Fed chairman in that situation is to resist the political pressure. Lucky for you, the next Fed Open Market Committee meeting is not scheduled until May 6-7—a cut then would at least allow the appearance that it’s not caving in to Trump’s demand.

And privately—you might not want to advertise this—you know that Trump might be right.

Definitely the “late” and “slow moving” parts touch a nerve. The Fed kept the federal funds rate at zero all the way into March 2022 when Consumer Price Index Inflation was at 8.5 percent. It prompted conferences, academic papers, think-tank reports. The Manhattan Institute issued a March 2024 paper: “Reform the Federal Reserve’s Governance to Deliver Better Monetary Outcomes.” One author, Dan Katz, is now chief of staff at the U.S. Treasury. The other, Stephen Miran, is now chair of the president’s Council of Economic Advisers. They want to change the law so that elected state governors will choose the regional Fed bank chairs, and also to clarify that Fed governors serve at the will of the U.S. president.

And the inflation data justifies a cut. Scott Grannis, who has been consistently right and whose charts and commentary are available free on the web without having to pay Goldman Sachs or for a Bloomberg terminal, has a March 13 update: “I detect no reason to worry about inflation.” You can get technical about it—“owner’s equivalent rent” as part of shelter costs—but why get into the weeds? Grannis writes, “Worry about growth, not inflation.” Makes sense. And that was before the latest stock market selloff and the tariffs’ effect on foreign tourism to the U.S. And before the disruption from the unwinding of highly leveraged Treasury basis trades.

Typically the Fed deals with inflation by raising rates to cool the economy and slow demand-fueled inflation. But any inflationary consequences of the tariffs are more like the supply-chain shocks that, during the pandemic, Fed officials called “transitory.”

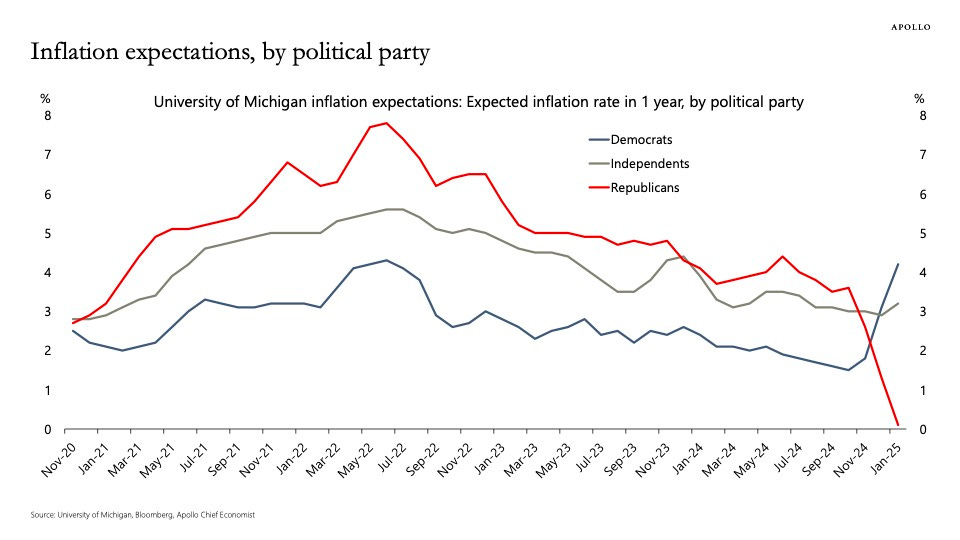

Everything is tribal, political, and brutal, and financial markets are operating against this backdrop which, if anything, has gotten more brutal in the past two months. Look at the University of Michigan data on the difference in inflation expectations between Democrats and Republicans, and the way it reversed between before and after the presidential election.

The former president of the Richmond Fed, Jeffrey Lacker, went into great detail in a highly illuminating February 2024 podcast about the Fed’s inner workings. “Chair Powell prefers the operations and the norms of a corporate board in which maybe you dissent internally, you express different views within the committee walls, or maybe even not then,” Lacker says. “Outside, you present a united front.”

A paper by Gauti Eggertsson and Don Kohn, a longtime Fed veteran, said, “The FOMC has had a very consensus-driven decision process. The committee should ask itself whether different aspects of its decisions and decision-making are allowing sufficient scope for effective challenges to the majority view.”

Lacker praises Kohn for his habit of hearing the other views: “He would do this thing people talk about in marriage counseling about active listening.”

Powell is the consensus-maker, playing the regional Fed bank presidents like a calliope.

But after being slow to fight inflation in 2021 and 2022, the worst thing for the Fed would be to be slow again, this time in heading off a potential recession that would violate the maximum employment part of the Fed’s dual mandate. Maybe it’s ironic, but it could be that the best thing you, Chairman Powell, could do—not just for the American economy, but for the Fed and its institutional independence—is listen to the president.

If the tariffs continue, they will create inflation, prompting interest rate increases.

If the tariffs continue, they will slow the economy, prompting interest rate cuts.

It is not simple to predict whether the tariffs continue, and if they do, which effect will dominate and require which change in interest rates.

I don't know how you can be so confident in what comes next. Uncharted territory.