What I Said at the State Hearing on Harvard’s $2 Billion Tax-Exempt Bond Offering

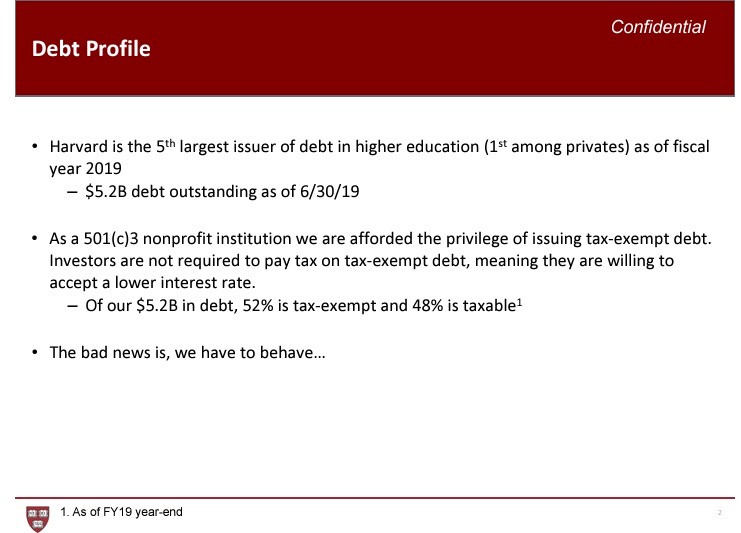

”The bad news is, we have to behave,” says a Harvard slide labeled ”confidential”

One of the consequences of the collapse of the press that I wrote about yesterday (“The Last Los Angeles Times Press Run”) is that newsworthy events, such as yesterday’s public hearing of the Massachusetts Development Finance Agency board on Harvard’s $2 billion tax exempt bond financing, don’t get news coverage. As context, $2 billion is more than the entire amount of bond financing this agency has issued statewide in recent calendar years. The entire Fidelity Massachusetts tax-exempt bond fund is about $2.6 billion and the Vanguard one is about $2.6 billion so $2 billion is just a lot of Massachusetts tax-exempt bonds.

I testified at the hearing. Here’s what I said:

I am a journalist, Massachusetts taxpayer, and Harvard alumni volunteer. I was employed by the university from 2019 to 2023. I am also a member of the Harvard Jewish Alumni Alliance.

I’m not a bond lawyer, yet as I understand it, under Massachusetts law, to authorize this bond offering you must determine that Harvard is a “responsible party.” I urge you, in considering whether Harvard meets that legal requirement, to use not some narrow technical financial definition of “responsible” about whether Harvard will or won’t be able to pay back this borrowed money, but to rather include in your consideration the definitions of responsible in my Webster’s Second Unabridged dictionary of the English language: “able to distinguish between right and wrong and to think and act rationally, and hence accountable for one’s behavior” and “trustworthy, dependable, reliable.”

In area after area, but most dramatically in the area of antisemitism and the response to the October 7 Hamas terrorist attack on Israel, Harvard has demonstrated itself to be not responsible, but rather irresponsible.

As a result, I respectfully ask you to consider delaying the approval of this bond offering so that Harvard can correct and improve its behavior.

Approving the full amount of this bond offering would only reward Harvard’s irresponsible behavior. It would send a message to the world that a university can permit and encourage egregious Jew-hate and discrimination—and then be rescued by Massachusetts taxpayers.

Antisemitism and Jew-hate.

Harvard has a well-documented history of Jew-hate dating back centuries, including discriminatory quotas in admissions that were acknowledged though not formally apologized for as part of Harvard’s slavery report. In 2022, an external report found Harvard worst in the nation in antisemitism, and I was quoted publicly as a Harvard employee saying, “having been around the university now on and off for more than 30 years, the level of antisemitism on campus over the past year is shocking, embarrassing, disgraceful—like nothing I’ve seen before. All of us who care about the University really need to work urgently to improve the situation or else face a real risk of Harvard losing Jewish talent and excellence to other, less hostile institutions.”

Since October 7, this has been the subject of extensive press attention, lawsuits, and bipartisan investigations by Congress and the U.S. Department of Education. It contributed to the resignation of Harvard President Claudine Gay. Rather than forthrightly confronting the problem, Harvard’s leaders have tried to minimize it. The new interim president, Alan Garber, who helped manage Harvard into this crisis, appointed as co-chair of an antisemitism task force a professor who has twice claimed publicly that student complaints about antisemitism are “exaggerated.”

All this caused Harvard’s former president, a current professor at the university and a former U.S. Treasury secretary, Larry Summers, to declare on January 21, 2024, “I have lost confidence in the determination and ability of the Harvard Corporation and Harvard leadership to maintain Harvard as a place where Jews and Israelis can flourish.” Summers also said, “As things currently stand, I am unable to reassure Harvard community members, those we are recruiting or prospective students that Harvard is making progress in countering anti-Semitism.”

Since then, the situation has further deteriorated. The March-April issue of Harvard Magazine included an article by the editor referring to “alleged antisemitism,” as if there’s a doubt about it. The university’s official publication, the Harvard Gazette, poisons the campus atmosphere with regular demonization of Israel based on blatant inaccuracies. A March 5, 2024 column in the Crimson by Maya Bodnick, a current Harvard undergraduate, said, “Since interim University President Alan M. Garber ’76 took office, antisemitism has continued to thrive at Harvard. In the first two months of his presidency, Garber hasn’t done any better than his predecessor, former University President Claudine Gay, at addressing this explosion of hatred.” She wrote, “One of Garber’s primary responsibilities is tamping down on antisemitism. But he is failing.” Another Harvard student, Shabbos Kestenbaum, testified at a February 29, 2024, roundtable of the U.S. House Committee on Education and the Workforce that the antisemitism situation at Harvard has gotten worse, not better, since Alan Garber took over from Claudine Gay. As recently as today, March 12, a Harvard visiting scholar who resigned as a member of the antisemitism advisory committee, Rabbi David Wolpe, tweeted about how at Harvard, posters of Israeli hostages “did not survive a single night.”

The failure to stop or even to forthrightly acknowledge and apologize for discrimination against Jews shows that Harvard is not “responsible” in the sense of “able to distinguish between right and wrong,” “accountable for one’s behavior” or “trustworthy.”

General poor management.

The antisemitism scandal is only the latest to afflict Harvard in recent years. Among other highly publicized problems, the university has been found to have unlawfully discriminated against Asian-Americans in admissions; to have the morgue manager at Harvard medical school criminally charged with selling parts from bodies that had been donated for research and education purposes; had its fencing coach charged in a scheme related to selling his home at above market value to an athlete’s family; had various professors disciplined for sexual misconduct, and had research misconduct and plagiarism issues entangle various administrators and faculty members. Harvard may argue that its problems attract more attention or that it is a large and decentralized institution that for the most part is problem-free, but that is the same arrogant, defensive, denial posture that has afflicted the university’s response to the antisemitism crisis.

Poor financial management.

In February, Harvard made a “voluntary notice of potential issuance of bonds” that mentioned “up to approximately $900 million of tax-exempt fixed rate bonds….issued by the Massachusetts Development Finance Agency.” Barely a few weeks later, the Massachusetts Development Finance Agency public notice mentions an amount “not to exceed $2,000,000,000.” What accounts for more than doubling the borrowing amount?

Likewise, the prospectus for the taxable bonds issued by Harvard earlier this month states “the total outstanding amount of indebtedness is expected to be approximately $6.892 billion.” Harvard magazine says “total bonds and notes outstanding in the vicinity of $7.2 billion as of June 30, 2024.” If Harvard borrows $2 billion, will it be the biggest debtor in American higher education? Harvard’s September 2023 financial report said expenses rose at a rate “double the increase in revenue,” which it said, “is not sustainable.” Why is Harvard borrowing more (and adding interest expense) rather than addressing its cost issues? How would the endowment tax increases proposed by some legislators and the Trump campaign affect the ability to repay?

One of the projects listed for financing is a new economics department building. But Harvard announced in 2021 that Penny Pritzker “has made a $100-million commitment to build a new home for the economics department.” Why does Harvard need to borrow tax-free money to build this building when it has $100 million from Pritzker? Many of the Harvard economics faculty have offices elsewhere, anyway—some of them work at the National Bureau of Economic Research or in privately rented office space elsewhere in Harvard Square (Raj Chetty’s “Raj Mahal”) where they can accept grant money without paying exorbitant overhead to support Harvard’s vast bureaucracy. The Boston area is full of vacant Class A office space, and most places are reducing their footprints rather than building more space, in an era of hybrid and remote work. If the economists need space let them take the Red Line to the Federal Reserve building downtown, where the Harvard Management Company is sitting on plenty of surplus space with fine views of the harbor, and where market-oriented businesses to study are easily at hand. Perhaps they can help the endowment stop underperforming their Ivy League peers.

Harvard has publicly posted on its website a “tax exempt debt compliance primer” labeled “confidential” that says “the bad news is, we have to behave.” This exemplifies Harvard’s contemptuous attitude toward compliance—that having to follow the law is “bad news.” It notes that “private business use” in tax-exempt-financed spaces must be limited. A recent chair of the Harvard economic department reportedly earned $42 million in royalties from an economics textbook. Perhaps he wrote it from his house on Nantucket, but can Harvard really assure the board with any sincerity or confidence that “private business use” in a building full of highly skilled economists, many with lucrative consulting work, will be as limited as the law requires?

For all these reasons, I urge the board to consider delaying the bond offering until Harvard can better demonstrate that it meets the legal requirement of being a “responsible party.” I hope this happens rapidly, but it may require additional leadership changes or governance reforms.

Thank you for your consideration.

Law school faculty campaign contributions: A professor of law at Notre Dame Law School, Derek T. Muller, has analyzed the Federal Election Committee data on law professors. He looked at the years 2017 to early 2023 and found “3148 law faculty who contributed only to Democrats in this 5+ year span— 95.9% of the data set of those identified as contributing to either Democrats or Republicans in this period. Another 88 (2.7%) contributed only to Republicans.”

He goes on, “The dollar figures were likewise imbalanced but slightly less so. About $5.1 million went to Democrats in this period, about 92.3% of the total contributions to either Democrats or Republicans. About $425,000 went to Republicans.”

For all the talk about how the Federalist Society and the Law and Economics movement have been huge long term victories for conservative philanthropy, producing networks of conservative law professors, clerks, judges, Supreme Court justices, and opinions, the law school faculties still seem dramatically skewed in a pretty partisan direction.

As David Bernstein, a professor at George Mason University’s Antonin Scalia Law School, observed in a social media post, even the places that “have reputations as relatively conservative law schools” are overwhelmingly tilted to Democrats for campaign contributions. “This is what passes for relatively conservative in the academy,” Bernstein says.

Inflation: What the markets understand about inflation but the media doesn’t is that, as Scott Grannis, who runs the excellent Calafia Beach Pundit blog, puts it: “inflation is running hot only if you think it makes sense to look at the year over year rise in nationwide housing prices 18 months ago. If you omit that one item (which comprises about one-third of the CPI), then you find that the year over year change in the CPI has been less than 2% for the past 8 months.” As Grannis wrote earlier this week: “The world knows that inflation is under control and that sooner or later the Fed will begin reducing short-term interest rates.”

The alternative view is available in today’s Wall Street Journal editorial (“Hold the Inflation Champagne”) and in the gold and bitcoin prices. And Larry Summers has also been cautious.

But Grannis has been pretty reliable on this. Another voice consistently making the “inflation is over” argument is Alan Reynolds of the Cato Institute.

You’d think the liberal press would be pushing the “inflation is over” point, because it’s good political news for Biden. Maybe it’s too sophisticated an argument (involving technical questions about how the government statisticians measure imputed rents of owner-occupied housing, or “owner’s equivalent rent”, and actual rents of rental housing)? Or maybe the “bad news gets the clicks” outweighs “good news for Biden”? The Economist has a big piece on “America’s rental-market mystery and why it may deter the Federal Reserve from cutting interest rates,” confessing, “The details of how to calculate OER can seem abstruse.” Here at The Editors we try to make the abstruse understandable.

Democrats discover deregulation: Left-leaning Ezra Klein of the New York Times writes: “Tyler Cowen, the economist and Bloomberg columnist, is right when he says that the weakness of Biden’s economic agenda has been that it ‘has a lot of expenditure but very little deregulation.’ Even if Biden wins, he’s very likely to face a Republican Senate in 2025. Spending more money will be hard. But the money he’s already spending will go further, faster, if he cuts the red tape that makes it so hard to build homes, roads, factories and energy infrastructure. That requires a deregulatory agenda that can be a tough sell among parts of the Democratic coalition but might, just might, be possible as part of a deal with Republicans.”

I’m sure not hearing that deregulation message from Biden on the campaign trail, though Trump has been talking about it. If Biden listens to Klein about it, it wouldn’t be the first time Democrats pushed deregulation; I’ve written about President Carter, Senator Edward Kennedy, and Stephen Breyer and the roles they all played.

Bret Stephens on Israel: I don’t always agree with Bret Stephens of the New York Times, but he is having a good war, as the expression goes. His latest, “Israel Has No Choice but to Fight On,” is worth trying to get past the New York Times paywall for.

Thank you!: Thank you to the hundreds of new readers, subscribers and members here at the editors. If you like what we are doing, please forward this email to a friend and encourage them to sign up.

My oldest son applied to Harvard ten or so years ago. Didn’t get in but was close to it. Seeing what a mess it is there, I would not want any of my sons going there today.