Florida Catholic Schools See Enrollment Boom

Plus, “Crimson Courage” group tied to Democrats, Pritzker; Yale private equity sale

In this newsletter:

A new report highlights enrollment growth in Catholic Schools in Florida, where state policy includes school choice scholarships.

Who is behind “Crimson Courage,” an alumni group urging Harvard not to settle with the Trump administration? One key figure is part of the Pritzker family and has a track record of backing Harvard networks for political action in favor of Democrats and progressives.

Yale is reportedly closing on a deal to sell $2.5 billion in private equity holdings “at a discount,” Bloomberg reports. It’s being discussed in the context of financial pressure on higher education, but could also signal a broader trend of a run for the exits or at least reallocation away from private equity.

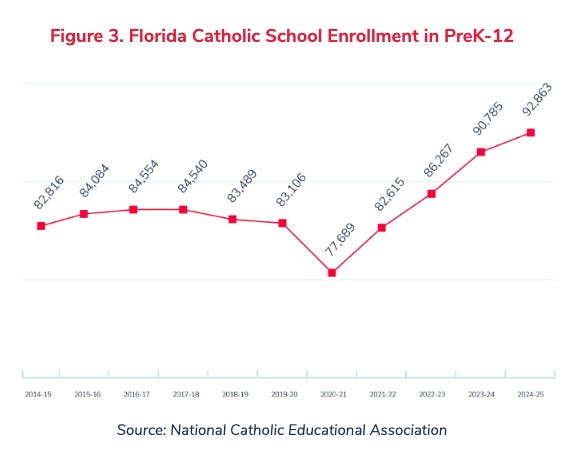

Florida Catholic Schools boom: While nationwide PreK-Grade 12 Catholic school enrollment declined 13.2 percent over the past decade, Catholic school enrollment in Florida is up 12.1 percent, a new report from the Florida Catholic Conference and Step Up For Students says.

School choice scholarships available under Florida law help make the cost of Catholic schools much closer to that of charter schools or public schools. “On a more level playing field, Catholic schools can compete,” the report says.

Some of the other states showing recent growth in Catholic school enrollment, such as Arizona, also have laws supporting school choice, while those that have seen sharp declines, like New York, do not.

The version of the One Big Beautiful Bill that passed the House of Representatives includes a new federal tax credit, capped at $5 billion a year, “for charitable contributions to tax-exempt organizations that provide scholarships to elementary and secondary school students.”

Florida’s Jewish schools have also benefited from the state scholarship program. Dan Senor gave a terrific speech the other day suggesting, among other things, that Jewish philanthropists give more to Jewish day schools. I’m all for it, but the most efficient way to do it might be to get more states to enact laws like Florida’s that help level the playing field, financially, between public and private schools. People worry about the cost, but in almost every case the per-student cost of the scholarship is less than the cost to the taxpayers of educating a student in the government-run schools. And if the students wind up learning more and being more productive members of society, it can wind up as a gain.

“Crimson Courage” group has major Democratic ties: A new group calling itself “Crimson Courage” has been organizing Harvard alumni “to support Harvard’s independence despite financial and other unconstitutional threats from the federal government.” The group describes itself as “nonpartisan,” but the people involved so far have included a lot of Democratic politicians, including Governor Maura Healey of Massachusetts, Lt. Gov. Antonio Delgado of New York, and former secretary of state Miles Rapoport of Connecticut. Also involved is Jessica Tang, the president of the American Federation of Teachers of Massachusetts; and a former Obama administration Justice Department official, Anurima Bhargava.

Donations to Crimson Courage go to the Foundation for Civic Leadership. Tax records show that the president of the Foundation of Civic Leadership, based in Cambridge, Mass., is Ian Simmons, who also gave the Foundation a $2,296,646 loan. Simmons runs a family office with his wife, Liesel Pritzker Simmons. (Penny Pritzker, a former Obama administration official from another branch of the Pritzker family, is the senior fellow of the Harvard Corporation, in effect the chair of Harvard’s board; J.B. Pritzker is the Democratic governor of Illinois. Liesel sued and won a reported $450 million settlement in 2005 in an intrafamily conflict over money.) Federal Election Commission records show Simmons has given more than a quarter-million dollars over the past few years to elect Democrats and defeat Donald Trump. He gave $45,000 to a group called “Crimson Goes Blue, Inc.,” and $2,000 to a group called Veritas Progressives Pac that spent money supporting canvassers in Maine and Pennsylvania. Veritas, or “truth,” in Latin, is Harvard’s motto.

Trump’s criticism of Harvard is partly that it has abandoned its research and teaching mission to become a political activist arm of the Democratic Party. Crimson Courage may think it is supporting “Harvard’s independence,” but it may actually be undermining it by demonstrating that Trump’s criticism has an element of truth to it.

Yale private equity sale: Yale “is finalizing the sale of as much as $2.5 billion” in private equity assets, “with an overall discount expected to be less than 10%, according to people with knowledge of the discussions, who asked not to be identified because the information is private. Potential buyers had valued parts of the portfolio at a haircut of as much as 15%, some of the people said,” Bloomberg reports (more nice work by The Great Janet Lorin and her colleagues).

The context in the Bloomberg story is mostly a potential increased endowment tax, an aspect of the Republican pressure on “elite” higher education. It’s somewhat comical that now that Congress is going to tax this stuff more, Yale is suddenly discovering, or admitting, that it’s worth less than it had previously claimed. It’s a little like Donald Trump telling his bank that his real estate is worth a lot, while claiming to New York for property tax purposes that it is worth less. When the purpose is telling U.S. News and prospective students or faculty members how solid the university is financially, a large endowment is good. But when the tax collector approaches, a large endowment, or at least one generating taxable payouts, is less good.

(On the endowment humor front, feature also Harvard publicly claiming that 80 percent of its endowment is restricted, but, in a recent subject-to-perjury-prosecution court filing, downgrading that to 70 percent. There are some subtleties and technical details involving whether the restriction applies to the purpose or the payout rate, but even so, it’s pretty rich material.)

To some significant extent this is less an exclusively higher education story, and more a finance story generally. One of the consequences of the Federal Reserve’s oppositional policy on short interest rates may be the exacerbation of the buildup and backlog of companies trapped in suspended animation in private equity, venture, and real estate funds. The exits are slowing, so instead of cash money distributions the investors might get a “continuation fund.”

If Yale, which is a sophisticated investor, is selling its private equity now even at a modest discount, maybe Yale figures that if they hold on to it and then have to sell it in a year or two, they might be stuck selling it at an even greater discount. If they thought the stuff was about to become extremely valuable, why would they dump it now? If they need liquidity, let them borrow against it, or try to.

There are plenty of smart and hardworking people in private equity, some of them readers of The Editors. Some savvy investors may make money buying this stuff from Yale or Harvard or other places at a discount in the secondary market, like distressed or vulture investors. But the Yale-David Swensen story that you can outperform public markets long-term by allocating a lot to private equity is a story that even Yale is now backing away from. The private equity funds will find other limited partners, either around the Arabian Gulf or among retail customers. And the endowments and pension funds won’t all abandon private equity immediately or entirely. But you can see the page turning.

Swensen, Yale’s chief investment officer, died of cancer in 2021 at age 67 and so is not around to see his university unwinding some of what he built, or to explain it in a way that would lead so many other money managers to try to follow. It was a great trade on the way up, and it doesn’t diminish Swensen’s legacy—and it may only burnish it— to observe that it is unlikely to be reproduced any time soon.

It would be good to get some sense of which of these are Yale's motivations in reducing its private equity stake:

1. Needing cash

2. Tax treatment of private equity versus other investments now that universities are expecting a tax increase

3. Concern that private equity stakes will decline in value